The Powerful Benefits of Tax-Deferred Growth and Tax-Free Withdrawals¹

Tax-deferred growth potential for faster accumulation

The money you earn in a 529 plan is not subject to federal or state income taxes, as long as it remains in the plan. This can help your account grow faster since all of your earnings can be reinvested, increasing returns with tax-free compounding.

Withdraw earnings without being taxed

No taxes are due to the federal government, or to most states, when money is withdrawn from a 529 account and applied to qualified expenses. And the list of what and where an expense counts as qualified is bigger than you might think. 529s can actually be used by almost anyone to pay for a host of education-related expenses.

529 Plan account owners can withdrawal assets to pay for K-122 tuition (public, private or religious) up to $10,000 per year per beneficiary. Always consult a tax professional; K-12 withdrawals may be subject to specific state taxes.

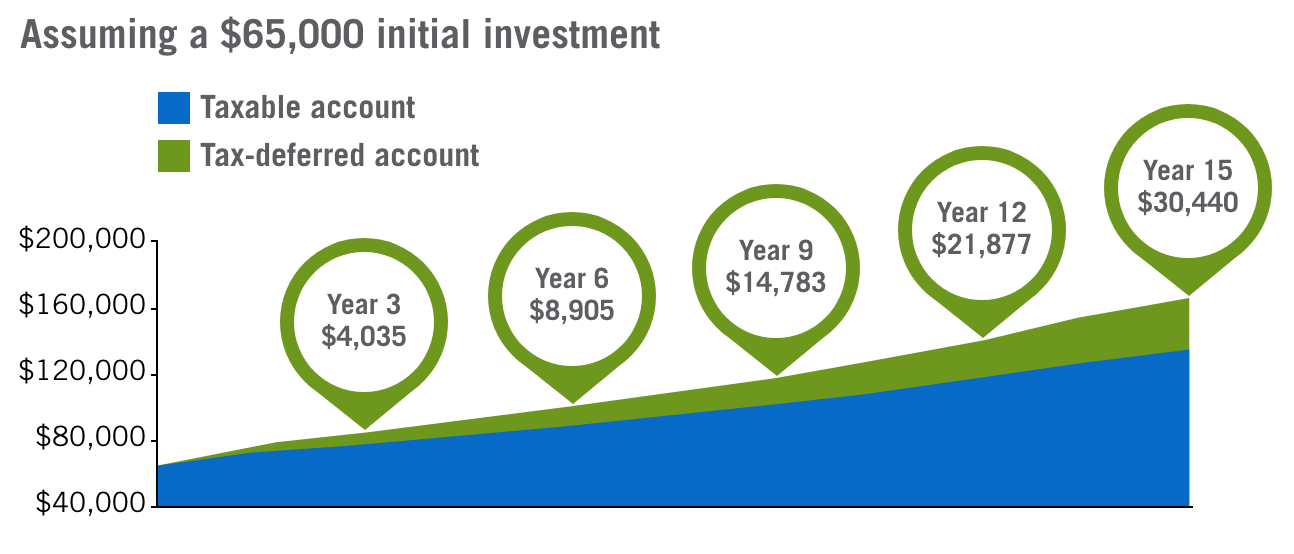

The power of tax-deferred growth potential

529 plans provide compounding growth potential in a tax-deferred account, which may provide substantially more growth potential over time than a taxable account.

The returns are hypothetical and do not represent the performance of any investment. This illustration assumes that no withdrawals are made that would not qualify as educational expenses. It is intended to compare a taxable investment account and a 529 tax-deferred account under the following assumptions: A) one lump-sum contribution of $65,000 of after-tax amounts is invested and all earnings, gained an annual average rate of 6.5%, compounded annually, are continually reinvested; and B) the taxable account is subject to an annual income tax on earnings at an aggregate rate of 30% (which may be both federal and state). No assumptions are made as to the disposition of the accounts following the 10th year.

Section 529 Qualified Tuition Programs are intended to be used only to save for qualified education expenses. These Programs are not intended to be used, nor should they be used, by any taxpayer for the purpose of evading federal or state taxes or tax penalties. Taxpayers may wish to seek tax advice from an independent tax advisor based on their own particular circumstances.

1 Withdrawals which are not for qualified educational expenses may be taxed as ordinary income and may be subject to a federal 10% additional tax.

2 K-12 tuition (public, private, or religious) up to $10,000 in tuition per year per beneficiary. Always consult a tax professional. K-12 withdrawals may be subject to specific state taxes.